Keep up with the latest cybersecurity threats, newly discovered vulnerabilities, data breach information, and emerging trends. Delivered daily or weekly right to your email inbox.

Voice, Proximity Key To Cutting<br>E-Payment Fraud

While we wait for EMV, US companies should lay the groundwork for strong security.

4 Min Read

In my previous column, I talked about US adoption of EMV (the Europay, MasterCard, and Visa initiative) and how it can help reduce fraud when data is stolen from merchants or card payment processors. However, EMV alone can't solve the problem.

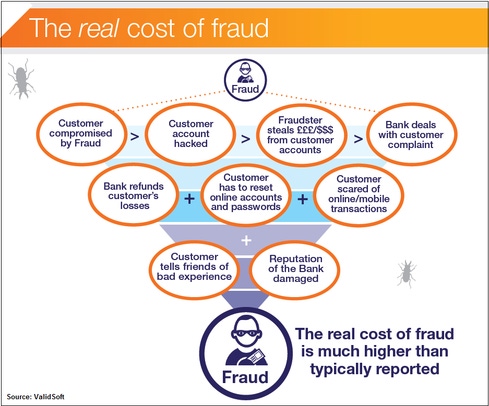

And the problem? It's severe. The 2013 LexisNexis True Cost of Fraud Study says merchants paid $2.79 for each dollar of losses they incur, up $0.10 on the dollar from 2012. Last year, the United States accounted for 47% of global fraud, while processing just 24% of payments by volume, according to the Nilson Report. In response, as I previously discussed, some non-US issuing banks are declining transactions on a massive scale, even though most are on the up and up. When a legitimate transaction is declined -- called a "false positive" in the trade -- costs can be 2-3 times higher than the actual potential fraud figure, and that doesn't include lost customer goodwill for someone standing at a checkout and having a card declined. The infographic below shows where that money goes.

Let's start with two points.

First, countries that have adopted EMV have enjoyed significant reductions in domestic and cross-border "card present" (at an ATM or a point of sale) fraud when the card is used in an EMV country. (The UK represents a terrific case study on EMV migration, and the fraud statistics before, during, and after are a very interesting read.) However, globally, we've also witnessed a significant increase in "card not present" fraud, such as during online purchases or mobile-device-based transactions, that isn't solved by EMV. While it clearly has a strong role to play in solving the problem of card present fraud, EMV alone won't reduce total payment card fraud, in the US or elsewhere.

Meanwhile, against the background of US EMV adoption, a payment revolution is occurring. I'm talking about the rise of contactless card payments (also known as "tap and go") and contactless mobile payments via mobile devices. Both are about as customer friendly and convenient as it gets, so it's no surprise they're among the fastest-growing payment methods.

However, these technologies bring their own security problems. For example, contactless technology (typically based on the ISO 14443 standard) introduces increased fraud risk, because no PIN or signature is required.

Fortunately, the EMV standard has evolved to include specifications for contactless and mobile payments. In addition to the standard EMV security model, the EMV contactless security model incorporates an extra digital certificate for signing contactless data and an extra master key to encrypt the cardholder's transmitted data.

EMV is not a prerequisite for secure contactless card payments. However, there's no reason it can't be combined with emerging security technologies to address the fraud issue, thereby enabling secure contactless card and mobile transactions. That could spell profit -- today, contactless card use tends to be limited to low-value transactions.

Fraud protection layers

Retailers need a multi-layered defense system that includes not only conventional data security mechanisms but also novel ways to authenticate users. That's so regardless of which channel or protocol they choose: EMV, RFID, NFC, or any other technology.

One possible approach to this authentication challenge that is already being adopted involves invisible, real-time, multilayer authentication systems featuring voice biometrics and/or location proximity (proximity correlation) technology.

It may seem like science fiction, but financial firms, including Wells Fargo, US Bank, and Barclays, use a customer's voice to authenticate transactions, as opposed to forcing them to type passwords on small screens. It's a natural as people become accustomed to interacting with mobile devices verbally.

Proximity correlation involves knowing that two elements are close to each other (in proximity) but with no detail shared as to where the party actually is, so privacy concerns are alleviated. This is very different from geolocation, where there's absolute clarity on where the party to a transaction actually is. Companies such as FICO and the Mastercard/Syniverse partnership have recently announced proximity capabilities.

Today, we're forcing a choice between security and convenience. But it doesn't have to be this way. The combination of a contactlesspayment card or smartphone and voice biometrics or proximity correlation provides convenience and security.

EMV is not a prerequisite -- these technologies are here today and could virtually eliminate fraud and false positives. Neither are they mutually exclusive. In fact, they're highly complementary. Proximity correlation can address those fraud situations not covered by EMV, such as stolen card + PIN, or stolen card + forged signature. Best of all, both voice biometrics and proximity correlation work as well, if not better, for mobile payments as they do for payment cards, so investments are forward looking and protected. EMV can follow in due course, and the savings to the industry over the next 2-3 years might just pay for the investment needed for EMV.

About the Author(s)

You May Also Like

More Insights

Webinars

Beyond Spam Filters and Firewalls: Preventing Business Email Compromises in the Modern Enterprise

April 30, 2024Key Findings from the State of AppSec Report 2024

May 7, 2024Is AI Identifying Threats to Your Network?

May 14, 2024Where and Why Threat Intelligence Makes Sense for Your Enterprise Security Strategy

May 15, 2024Safeguarding Political Campaigns: Defending Against Mass Phishing Attacks

May 16, 2024

Events

Black Hat USA - August 3-8 - Learn More

August 3, 2024Cybersecurity's Hottest New Technologies: What You Need To Know

March 21, 2024